Our investment committee does not put much value on economic forecasts. Ask us if we are headed to a recession, a soft landing, or continued growth in the economy and our answer is likely “we don’t know”. It is not that we don’t pay attention to weekly updates on jobs, manufacturing, retail sales, etc., but […]

Risk happens fast. Or does it? We believe risk is always present, it just rears its ugly head at different times for investors. Stocks finished last week with one of the largest weekly drawdowns since April. The S&P 500 sold off more than 2% while the tech-heavy Nasdaq gave up more than 3% in five […]

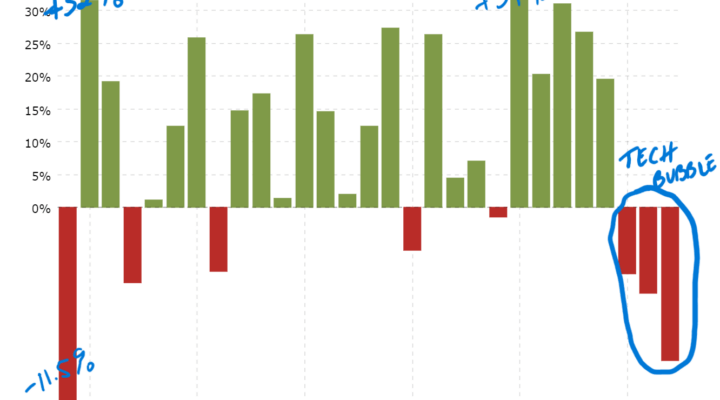

As the year progresses past the halfway point, I’d like to highlight some market dynamics which we think will become common themes in the second half of the year. Most importantly, the significant one-sidedness in outperformance from the largest public companies, mostly in the tech sector, has created an extremely top-heavy market. What exactly does […]

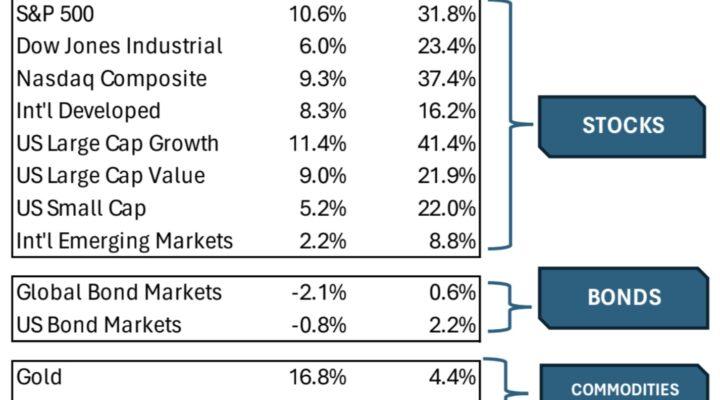

The principles of prudent investing involve broad diversification and the patience to stay the course, regardless of short term volatility. However, diversification across geographies, market capitalization (size of companies), and value versus growth companies (think Johnson & Johnson versus Netflix), did not help investors keep pace with the most widely followed and quoted stock index, […]

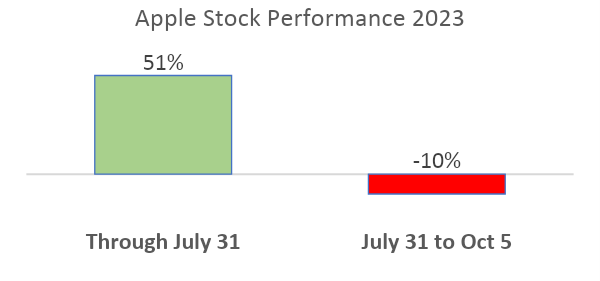

The start of the fourth quarter has been rough for financial markets, a follow-through from when stocks hit a 12-month high in July. The factors contributing to the sell-off: All is not dire, however. Financial markets look ahead and so do we . . . below is our stance on the issues outlined above:

How challenging was 2022 for investors in the US? Stocks and bonds have not produced negative returns of this magnitude, in the same calendar year, for more than fifty years. The closest parallel to the previous twelve months is the late 1960s/early 1970s, because the volatility is almost entirely due to inflation. That was a […]